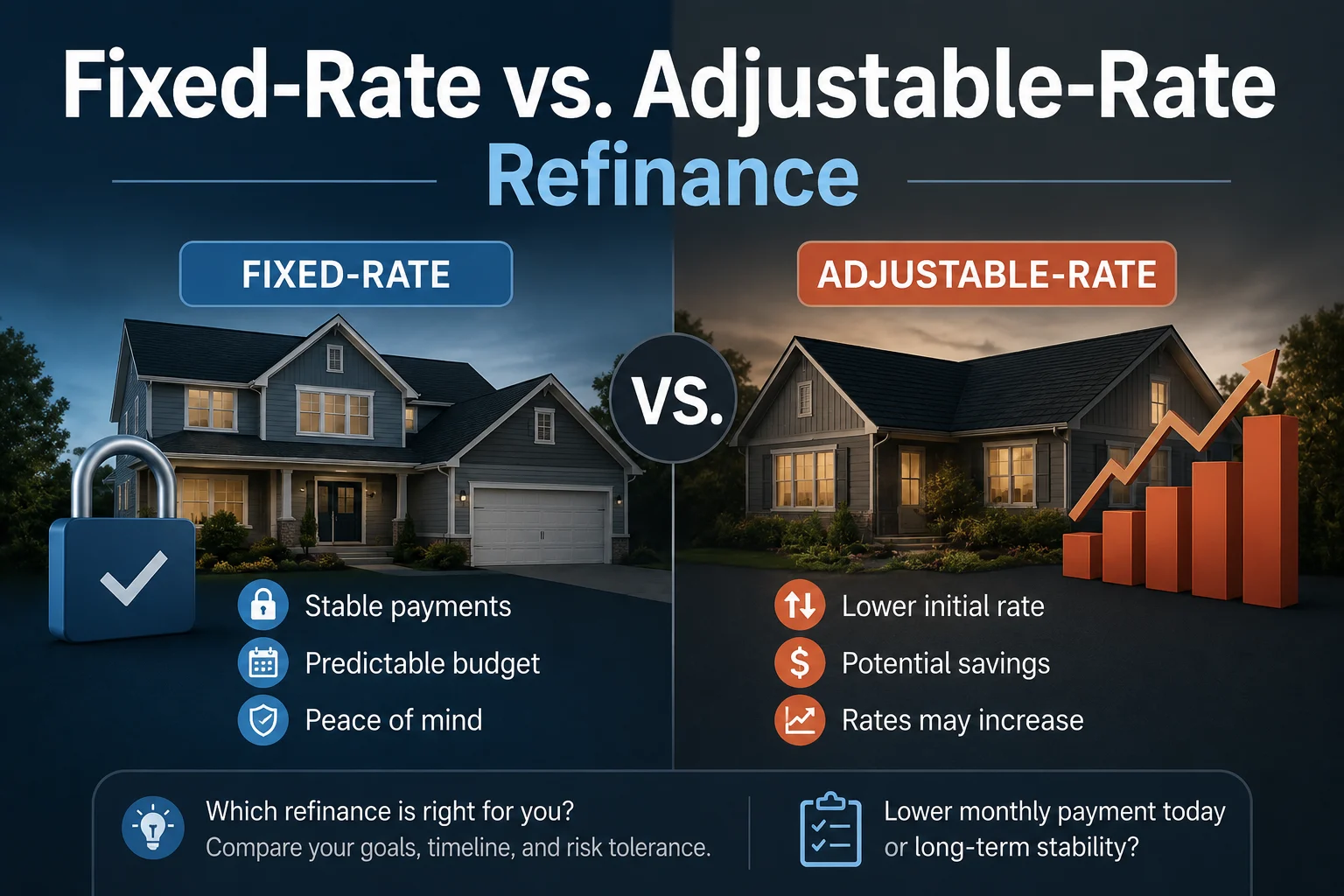

Introduction: One of the Most Important Mortgage Decisions You Will Ever Make

When homeowners decide to refinance their mortgage, they quickly discover that the decision involves far more than simply finding a lower interest rate. One of the most consequential choices they face — and one that is frequently misunderstood or rushed — is whether to refinance into a fixed-rate mortgage or an adjustable-rate mortgage.

This single decision can mean the difference between saving tens of thousands of dollars and paying tens of thousands more than necessary. It can mean the difference between a mortgage payment that stays predictable for decades and one that surges unexpectedly, straining your budget and threatening your financial stability.

And yet, despite how significant this choice is, most people make it with only a surface-level understanding of how these two mortgage types actually work — guided primarily by whichever option happens to offer a lower rate at the moment of application.

That approach is not good enough.

This comprehensive guide will give you everything you need to make this decision with confidence. We will break down exactly how fixed-rate and adjustable-rate mortgages work, compare their costs, risks, and benefits across real financial scenarios, examine the market conditions that favor each option, and help you build a clear framework for determining which refinance type genuinely fits your financial life — not just today, but for the years ahead.

Whether you are refinancing for the first time or reconsidering a past decision, this guide will give you the clarity and the tools to choose wisely.

Understanding the Two Options: A Foundation

Before comparing the two, it is essential to understand precisely what each option is and how it functions.

What Is a Fixed-Rate Mortgage?

A fixed-rate mortgage is a home loan in which the interest rate remains constant — completely unchanged — for the entire life of the loan. Whether that loan term is 10, 15, 20, or 30 years, the rate you lock in on day one is the rate you will pay on day 3,650 or day 10,950.

This means your principal and interest payment never changes. Your monthly mortgage obligation is completely predictable from the day you close to the day you make your final payment.

Fixed-rate mortgages are the most common mortgage type in the United States and many other countries. Their appeal is straightforward: certainty. In a world of economic volatility, the assurance that your largest monthly expense will not increase is enormously valuable — both financially and psychologically.

Common fixed-rate loan terms:

- 30-year fixed (most popular — lower monthly payments, higher total interest)

- 20-year fixed (middle ground — moderate payments and interest)

- 15-year fixed (higher monthly payments, significantly less total interest)

- 10-year fixed (highest payments, least total interest)

What Is an Adjustable-Rate Mortgage (ARM)?

An adjustable-rate mortgage — commonly called an ARM — is a home loan in which the interest rate is fixed for an initial period and then adjusts periodically based on a market benchmark index, plus a margin set by the lender.

ARMs are defined by their adjustment structure, typically expressed in a format like 5/1, 7/1, or 10/1:

- The first number represents the initial fixed-rate period in years (5, 7, or 10 years)

- The second number represents how frequently the rate adjusts after the fixed period (every 1 year is most common; some ARMs adjust every 6 months)

So a 5/1 ARM has a fixed rate for the first 5 years, then adjusts once every year after that. A 7/6 ARM is fixed for 7 years, then adjusts every 6 months.

After the fixed period ends, your rate — and therefore your monthly payment — can go up or down based on the movements of the index your loan is tied to. In the United States, most modern ARMs are tied to the Secured Overnight Financing Rate (SOFR), which replaced the London Interbank Offered Rate (LIBOR) as the primary benchmark in 2023.

ARM rate caps are critical consumer protections built into the loan that limit how much the interest rate can move:

- Initial adjustment cap — limits how much the rate can change at the first adjustment (typically 2% to 5%)

- Periodic adjustment cap — limits how much the rate can change at each subsequent adjustment (typically 1% to 2%)

- Lifetime cap — the maximum the rate can ever increase above the initial rate over the life of the loan (typically 5% to 6%)

Understanding these caps is essential to calculating your worst-case scenario under an ARM.

The Core Trade-Off: Certainty vs. Cost

The fundamental tension between fixed-rate and adjustable-rate mortgages comes down to a single trade-off:

Fixed-rate mortgages offer certainty at a cost. Adjustable-rate mortgages offer a lower initial cost at the price of certainty.

Fixed-rate mortgages typically carry higher interest rates than ARM initial rates. This premium reflects the value of the certainty they provide — the lender is assuming the risk that market rates will rise over the loan term, and they price that risk into your fixed rate.

ARMs typically offer lower initial rates — often 0.5% to 1.5% below comparable fixed-rate products — because the lender is transferring the interest rate risk to you. If rates rise, you bear the consequences through a higher payment. If rates fall, you benefit through a lower payment.

The question refinancing homeowners must answer is not which option has a lower rate today. It is the option that serves their specific financial situation, timeline, and risk tolerance over the life of their loan.

Fixed-Rate Refinance: The Full Picture

Advantages of Refinancing Into a Fixed Rate

1. Absolute Payment Predictability

Your principal and interest payment is locked. No matter what happens to inflation, the Federal Reserve’s interest rate decisions, the bond market, or the broader economy, your mortgage payment does not move. For households managing tight budgets, supporting families, or planning for retirement on a predictable income, this predictability is not just convenient — it is foundational to financial planning.

2. Long-Term Interest Rate Protection

If you refinance into a fixed rate during a period of historically low or moderate rates, you lock in that rate for the entire loan term. If rates rise significantly in subsequent years — as they did dramatically between 2022 and 2024 — you are completely insulated. Your neighbors who chose ARMs may see their payments surge while yours stay unchanged.

3. Simplicity and Transparency

Fixed-rate mortgages are simple to understand and straightforward to plan around. There are no calculations about index rates, margins, or adjustment caps. You know exactly what you owe every month, every year, for the life of the loan. This simplicity has real psychological and administrative value.

4. Equity Building Consistency

Because your payment never changes, the portion going toward principal follows a completely predictable amortization schedule. You always know how much equity you are building and at what rate — which matters enormously for long-term wealth planning.

5. Refinancing Protection in Low-Rate Environments

If you lock in a low fixed rate and rates subsequently rise, you have no incentive to refinance again — you already have the best available rate. This protects you from the transaction costs of serial refinancing.

Disadvantages of Refinancing Into a Fixed Rate

1. Higher Initial Interest Rate

Fixed rates are almost always higher than the initial rate on a comparable ARM. Depending on market conditions, this premium can be substantial — meaning your monthly payment under a fixed-rate refinance will be higher than under an ARM refinance, at least initially.

2. Less Beneficial in Declining Rate Environments

If you lock in a fixed rate and market rates subsequently fall, you are stuck at your higher rate until you refinance again — which involves additional closing costs and administrative effort.

3. Higher Total Interest if You Move or Refinance Early

If you sell your home or refinance again within a few years, you will have paid the higher fixed rate without benefiting from its long-term protection. In short-hold scenarios, a fixed rate may cost you more than an ARM would have.

4. Less Flexibility

Fixed-rate mortgages offer no built-in mechanism to benefit from falling rates without the friction and cost of refinancing. ARMs adjust automatically — for better or worse.

Adjustable-Rate Refinance: The Full Picture

Advantages of Refinancing Into an ARM

1. Lower Initial Interest Rate and Monthly Payment

This is the primary appeal of ARMs. The initial rate on a 5/1 or 7/1 ARM is typically significantly lower than a comparable fixed-rate product. This translates directly into lower monthly payments during the fixed period, which can generate meaningful cash flow savings, particularly on larger loan balances.

On a $400,000 refinance, the difference between a 6.75% fixed rate and a 5.75% initial ARM rate is approximately $265 per month. Over a 5-year fixed period, that is $15,900 in savings — before the ARM ever adjusts.

2. Ideal for Shorter Holding Periods

If you know — or strongly believe — that you will sell the home or refinance again before the ARM’s fixed period ends, you capture all the benefits of the lower rate with none of the adjustment risk. You leave before the uncertainty begins.

3. Built-In Benefit from Falling Rates

If market interest rates decline after your ARM’s fixed period ends, your rate adjusts downward automatically — without the need to refinance, pay closing costs, or take any action whatsoever. This automatic downward flexibility is a genuine advantage in declining-rate environments.

4. Useful in High-Rate Environments With Expected Rate Declines

When rates are elevated and widely expected to fall — such as after a Federal Reserve tightening cycle appears to be ending — an ARM can be a strategic choice. You capture a lower rate than the current fixed-rate market offers, and if rates fall as expected, your ARM may adjust downward even further.

5. Lower Effective Rate Over Medium-Term Holds

Even for homeowners who stay somewhat past the initial fixed period, an ARM can sometimes be cheaper over a 7 to 10 year horizon than a fixed-rate loan — if adjustments remain modest and the initial rate differential was large.

Disadvantages of Refinancing Into an ARM

1. Payment Uncertainty After the Fixed Period

This is the defining risk of an ARM. Once the fixed period ends, your payment can change — sometimes significantly — at each adjustment interval. For households with tight budgets or fixed incomes, this uncertainty can be financially and psychologically stressful.

2. Worst-Case Scenario Can Be Severe

If rates rise substantially during your ARM’s adjustment period, your payment can increase dramatically. Consider a homeowner with a $350,000 loan balance at a 5.5% initial ARM rate. With a 5% lifetime cap, the rate could ultimately reach 10.5%. At that rate, the monthly payment on the remaining balance could be $700 to $1,000 per month more than the initial payment — a potentially devastating increase.

3. Complexity and Ongoing Monitoring Required

Unlike fixed-rate mortgages, ARMs require ongoing attention. You need to monitor the index your rate is tied to, understand when your next adjustment is coming, calculate what your new payment will be, and determine whether refinancing into a fixed rate makes sense before the adjustment hits.

4. Refinancing Risk

If you plan to refinance out of your ARM before it adjusts, but market conditions change — rates rise significantly, your home value falls, or your credit deteriorates — you may be unable to refinance on favorable terms and find yourself stuck with a rising ARM payment.

5. Harder to Plan Long-Term Finances

Budget planning, retirement savings projections, and long-term financial modeling are all more complicated when a major monthly expense — your mortgage — is an uncertain variable. The psychological burden of this uncertainty is real and should not be underestimated.

The Critical Role of Market Conditions

The choice between fixed and adjustable rates cannot be made in isolation from the interest rate environment you are refinancing in. Market conditions dramatically influence which option makes more strategic sense.

Refinancing in a Low-Rate Environment

When mortgage rates are near historic lows — as they were between 2020 and 2021, when 30-year fixed rates briefly fell below 3% — refinancing into a fixed rate is almost always the superior choice for most homeowners. Here is why:

- The premium over ARM rates is minimal because fixed rates are already low

- The protection against future rate increases is extremely valuable because rates have little room to fall but significant room to rise.

- Locking in a generational low rate is a once-in-a-decade opportunity that may not recur for many years.

Homeowners who refinanced into 30-year fixed rates at 2.75% to 3.25% in 2020 and 2021 made one of the best financial decisions available to them. Those who chose ARMs in that environment gained very little from the lower initial rate while forfeiting the extraordinary certainty of a historically low fixed rate.

Refinancing in a High-Rate Environment

When rates are elevated — as they were during 2023 and 2024, with 30-year fixed rates reaching 7% to 8% — the calculus shifts. Here is why ARMs become more attractive:

- The rate differential between ARMs and fixed rates widens, making ARM savings more substantial

- If rates are high because of an aggressive monetary tightening cycle, there is a reasonable expectation that rates will moderate over the coming years — potentially benefiting ARM holders at adjustment.

- For homeowners who do not plan to stay long-term, enduring a high fixed rate for 30 years is a poor choice when an ARM offers a meaningfully lower rate for their realistic holding period

However, refinancing into an ARM in a high-rate environment carries a specific risk: if rates remain elevated or rise further, the ARM provides no protection. The decision must be made with clear eyes about the realistic range of rate scenarios — not just the optimistic one.

Refinancing During Rate Uncertainty

When the interest rate outlook is genuinely uncertain — as it frequently is — the decision becomes more personal than mathematical. It depends on your risk tolerance, your financial resilience, and your ability to absorb payment increases if they occur. In periods of uncertainty, fixed-rate refinancing tends to be the more prudent choice for the majority of homeowners, precisely because it eliminates the variable most difficult to predict.

Side-by-Side Comparison: Real Numbers Across Scenarios

Let us run through three real scenarios to illustrate how these options perform across different homeowner situations.

Scenario 1: Long-Term Homeowner, Stable Situation

Profile: Married couple, age 45. Remaining mortgage balance: $320,000. Plan to stay at home until retirement in 20 years. Combined income is stable and sufficient. Moderate risk tolerance.

Option A: 20-Year Fixed at 6.50%

- Monthly P&I payment: $2,387

- Total interest over 20 years: $252,900

- Certainty: Complete

Option B: 7/1 ARM at 5.75% (caps: 2/1/5)

- Initial monthly P&I payment: $2,255

- Monthly savings vs. fixed (first 7 years): $132/month

- Total savings during fixed period: $11,088

- After Year 7: Rate could rise to 7.75% in year 8 (if rates have risen). Payment could jump to $2,618/month — $363 more than the current ARM payment and $231 more than the fixed option.

- If rates rise to the worst-case cap of 10.75%: Monthly payment could reach $3,200+ — nearly $1,000 more per month than the fixed option

Verdict: For this couple, the fixed-rate refinance is the clear winner. The $11,088 savings during the ARM’s fixed period are more than offset by the payment risk over the remaining 13 years of their planned holding period. The certainty of the fixed rate aligns perfectly with their long-term horizon and the financial planning demands of approaching retirement.

Scenario 2: Short-Term Homeowner, Likely to Move

Profile: Single professional, age 32. Remaining mortgage balance: $275,000. Expects to relocate for career advancement within 4 to 5 years. High income, strong savings.

Option A: 30-Year Fixed at 6.75%

- Monthly P&I payment: $1,784

- Total paid over 5 years: $107,040 (mostly interest)

- Rate certainty: irrelevant — will sell before any risk materializes anyway

Option B: 5/1 ARM at 5.875%

- Monthly P&I payment: $1,627

- Monthly savings vs. fixed: $157/month

- Total savings over 5-year holding period: $9,420

- Risk: Rate adjusts after 5 years — but this homeowner will have sold before then

Verdict: The ARM is the clear winner here. This homeowner captures $9,420 in savings during their holding period and exits before the ARM ever adjusts. The 30-year fixed rate provides the certainty they do not need for a risk they will never face.

Scenario 3: Mid-Term Homeowner, Uncertain Timeline

Profile: Family with two children, age 38. Remaining balance: $380,000. Plans to stay in the home for approximately 8 to 10 years — but this is not certain. Income is good but includes variable bonuses.

Option A: 30-Year Fixed at 6.875%

- Monthly P&I payment: $2,497

- Certainty: Complete for full term

- Flexibility: None — stuck at this rate unless refinancing again

Option B: 10/1 ARM at 6.125%

- Initial monthly P&I payment: $2,310

- Monthly savings vs. fixed: $187/month

- Total savings during fixed period (10 years): $22,440

- Risk: Rate adjusts after year 10 — but family may have sold by then

- Worst case: If still in the home and rates have risen, the adjustment could add $300 to $700+ per month

Verdict: This is the genuinely difficult scenario — and the most common one. The 10/1 ARM offers $22,440 in savings and aligns reasonably well with the expected holding period. But the uncertainty in the timeline creates real risk. The right answer depends on this family’s financial resilience: if they could absorb a significantly higher payment post-adjustment without crisis, the ARM may be appropriate. If a $500 monthly payment increase would create genuine hardship, the fixed rate is the safer choice — even at a higher cost.

Key Questions to Guide Your Decision

When you sit down to make this choice, these are the questions that matter most:

How Long Do You Realistically Plan to Stay in the Home?

This is the single most important question. Be honest — not optimistic. Consider your career trajectory, family plans, life stage, and the realistic probability of relocation. If the answer is fewer than 5 to 7 years with reasonable confidence, an ARM warrants serious consideration. If the answer is 10 or more years, or genuinely uncertain, a fixed rate is likely the more prudent choice.

Can You Absorb a Significantly Higher Payment If Your ARM Adjusts Upward?

Calculate your worst-case ARM payment using the lifetime cap. Then ask honestly: If that payment were required of you, would your financial situation remain stable? Would you be able to continue saving for retirement, maintaining your emergency fund, and meeting other financial obligations? If the answer is no, the ARM’s risk is too great regardless of the rate savings.

What Is Your Risk Tolerance?

This is as much a psychological question as a financial one. Some people experience genuine anxiety about variable expenses they cannot fully predict. For them, the certainty of a fixed rate has a value that transcends pure financial calculation — the peace of mind is worth the premium. There is no shame in acknowledging this. A mortgage you can sleep with is better than a theoretically superior mortgage that costs you stress and sleep for years.

What Direction Are Interest Rates Likely to Move?

No one can predict rates with certainty — if they could, they would be extraordinarily wealthy. But you can form a reasonable view based on the current economic environment, Federal Reserve communications, inflation trends, and professional forecasts. If rates are high and likely to moderate, an ARM has additional appeal. If rates are low and likely to rise, a fixed rate deserves a premium.

How Large Is Your Loan Balance?

The larger the loan balance, the greater the dollar impact of any rate difference — in both directions. A 1% rate differential on a $150,000 balance is $1,500 per year. On a $600,000 balance, it is $6,000 per year. High-balance borrowers feel the stakes of this decision most acutely.

Is Your Income Stable and Predictable?

Homeowners with stable, predictable income — salaried employees, government workers, established professionals — can manage payment uncertainty more effectively than those with variable income. If your income fluctuates, adding mortgage payment volatility compounds your financial unpredictability in potentially dangerous ways.

Hybrid Strategies: Getting the Best of Both Worlds

For homeowners who feel genuinely torn, some strategies blend the characteristics of both loan types:

The ARM-to-Fixed Strategy

Some homeowners deliberately choose an ARM for the lower initial rate, with a pre-committed plan to refinance into a fixed rate before the ARM begins adjusting. This strategy captures the ARM’s initial savings while still securing long-term rate certainty — but it depends on favorable refinancing conditions being available when needed. If rates have risen significantly when the time comes to convert, the strategy may backfire.

Choosing a Longer ARM Fixed Period

A 10/1 ARM offers a 10-year fixed period — significantly longer than a 5/1 ARM. For homeowners with medium-term holding horizons (7 to 12 years), this can be the optimal middle ground: a lower rate than a fixed mortgage, with a fixed period long enough to cover most or all of the expected holding period.

Paying Down Principal Aggressively

Some homeowners choose an ARM but commit to making additional principal payments during the fixed period. This reduces the loan balance that will be subject to future adjustments and accelerates overall payoff — potentially exiting the loan entirely before the adjustment period becomes financially significant.

Shorter Fixed-Rate Term Instead of ARM

Rather than an ARM, some homeowners achieve a lower rate by choosing a shorter fixed-rate term — refinancing from a 30-year to a 15-year fixed. While monthly payments are higher, the interest rate is lower than a 30-year fixed, and the certainty is complete. This is worth comparing directly to ARM options before making a final decision.

The Refinancing Decision Framework: A Step-by-Step Guide

Use this framework to structure your decision methodically:

Step 1 — Establish Your Realistic Timeline: How long will you keep this loan? Be specific and honest. Write the number down.

Step 2 — Get Competing Quotes for Both Options. Request Loan Estimates for your best fixed-rate option and your best ARM option from at least three to five lenders. Compare them on an equal basis using the standardized Loan Estimate document.

Step 3 — Calculate the Break-Even on the Rate Differential. How long until the ARM’s lower payments accumulate savings equal to the fixed rate’s certainty premium? This tells you the timeline at which the two options are equivalent.

Step 4 — Stress-Test the ARM Calculate your payment at each cap level: initial adjustment cap, periodic cap, and lifetime cap. Can you afford the worst case?

Step 5 — Assess Your Risk Tolerance. Would payment uncertainty cause you meaningful financial anxiety? Would it impair your ability to plan? Factor this into your decision as a legitimate consideration.

Step 6 — Consider the Rate Environment: Where are rates in the historical cycle? Are they likely to rise, fall, or stay stable? Does this shift the balance toward one option?

Step 7 — Make Your Decision and Commit. Once you have run the analysis, make your choice with confidence. Refinancing paralysis — endlessly delaying a decision — is itself a costly mistake. A good decision made today beats a perfect decision made next year.

Common Mistakes to Avoid

Choosing solely based on the lowest advertised rate. A 5/1 ARM with a low teaser rate may look attractive in the advertisement, but it may be poorly suited to your 15-year holding horizon.

Ignoring the ARM caps. The initial rate is only the beginning of the ARM story. Always calculate the worst-case payment using the lifetime cap.

Assuming you can always refinance later. Many homeowners choose ARMs, planning to refinance before the adjustment hits — then find that falling home values, rising rates, or changed income make refinancing impossible or unfavorable. Never assume future refinancing as a guaranteed escape route.

Underestimating how long you will stay. People consistently underestimate their attachment to their homes and the friction involved in moving. If you think you will move in 5 years, add 3 years to that estimate before making your mortgage decision.

Choosing a fixed rate because it “feels safer” without running the numbers. For some homeowners in some situations, a fixed rate is genuinely the better choice. For others, that feeling of safety comes at a premium that is not justified by their actual situation. Run the numbers before relying on instinct.

Focusing only on the monthly payment. Total interest paid over your holding period matters enormously. A lower monthly ARM payment can cost more in total interest than a fixed rate, or vice versa, depending on your timeline and rate movements.

Final Verdict: Which Is Right for You?

After everything covered in this guide, here is the clearest possible summary of when each option makes sense:

Choose a Fixed-Rate Refinance if:

- You plan to stay in the home for 10 or more years

- You cannot comfortably absorb significant payment increases

- You are refinancing in a low or historically moderate rate environment

- You value certainty and predictability above all else in your financial planning

- You are on a fixed income or approaching retirement

- Your loan balance is large, and rate differences generate significant dollar impacts

Choose an Adjustable-Rate Refinance if:

- You have a clear, well-founded plan to sell or refinance within 5 to 7 years

- You can comfortably absorb worst-case payment increases without financial hardship

- You are refinancing in a high-rate environment with a reasonable expectation of rate moderation

- Your primary goal is to maximize cash flow during a defined period

- You have strong financial reserves and a high risk tolerance

- You are an experienced homeowner who will actively monitor and manage the loan

When in doubt: If you are genuinely uncertain about your timeline or risk tolerance, the fixed-rate refinance is the more prudent default for most homeowners. The certainty it provides has real financial and psychological value — and avoiding the worst-case ARM scenario is worth the premium in the majority of situations where the future is unclear.

The best mortgage is not the one with the lowest rate today. It is the one most precisely aligned with your real financial life — your timeline, your income, your risk tolerance, and your long-term goals.

Take the time to know your numbers, understand your options, and make your choice deliberately. Your future financial self will thank you for it.

Frequently Asked Questions (FAQs)

Q: Is a fixed-rate or adjustable-rate refinance better right now? A: It depends on current market conditions, your holding period, and your risk tolerance. In general, when rates are high and expected to fall, ARMs deserve consideration. When rates are low, locking in a fixed rate is usually superior. Consult current rate data and a licensed mortgage professional for personalized guidance.

Q: What happens if I cannot afford my ARM payment after it adjusts? A: Your options include refinancing into a fixed rate (if you qualify), requesting a loan modification from your lender, or, in extreme cases, selling the home. This is why stress-testing your worst-case ARM payment before committing is essential.

Q: Can I convert an ARM to a fixed-rate mortgage? A: Some ARMs include a conversion option that allows you to switch to a fixed rate at specific points in the loan term. Otherwise, you would need to refinance, which involves new closing costs and qualification requirements.

Q: How often does an ARM actually adjust in real life? A: Adjustment frequency depends on your specific loan structure (5/1, 7/1, 10/1, etc.). After the initial fixed period, most ARMs adjust annually. Some adjust every 6 months. Your loan documents specify the exact schedule.

Q: Is a 15-year fixed rate better than a 30-year fixed rate for refinancing? A: A 15-year fixed rate offers a lower interest rate and far less total interest paid — but requires a significantly higher monthly payment. It is superior for homeowners who can comfortably afford the higher payment and want to build equity rapidly. The 30-year fixed is better for those who prioritize monthly cash flow flexibility.

Q: What index are most ARMs tied to today? A: Most ARMs originated in the United States today are tied to SOFR — the Secured Overnight Financing Rate — which replaced LIBOR as the primary benchmark index in 2023.

Q: Should I refinance from an ARM to a fixed rate? A: If your ARM’s fixed period is ending and you plan to stay in the home long-term, refinancing into a fixed rate before the adjustment hits is often a smart move — especially if you can secure a rate meaningfully below your expected ARM adjustment rate.